UK borrowing at record high as virus cost soars in April

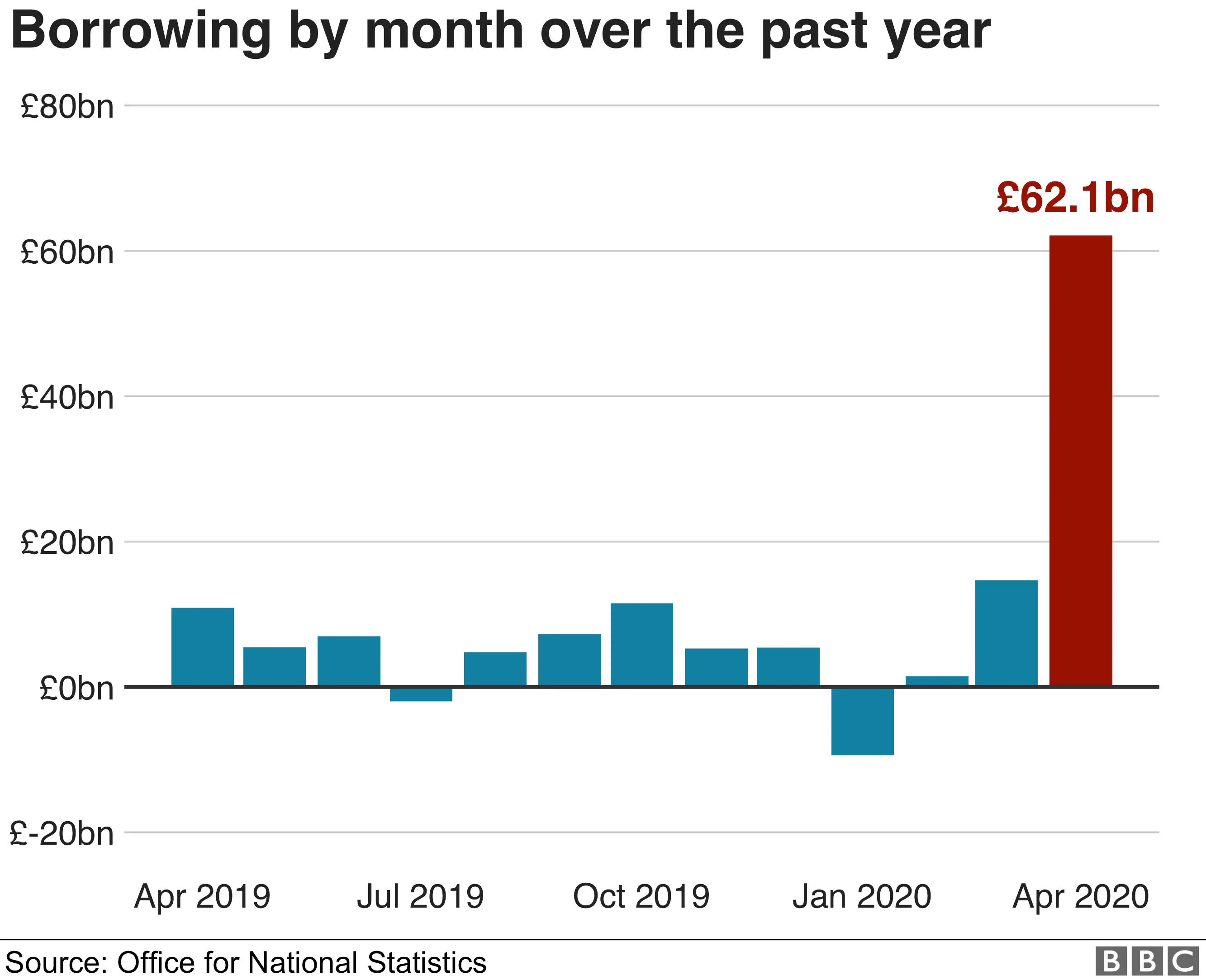

Government borrowing surged to £62bn in April, the highest monthly figure on record, after heavy spending to ease the coronavirus crisis.

It means the deficit - the difference between spending and tax income - was larger last month than forecast for the whole year at the time of the Budget.

The data from the Office for National Statistics revealed the soaring cost of support, such as furlough schemes.

But Chancellor Rishi Sunak said things would be worse without government aid.

The government's independent forecaster, the Office for Budget Responsibility (OBR), has predicted that borrowing for the whole year could reach £298bn, more than five times the estimate at the time of the March Budget.

Jonathan Athow, deputy national statistician at the ONS, described April's figure as "pretty much unprecedented". It said the cost of furlough schemes alone was £14bn in April.

"Borrowing now is about six times what it was [in April] last year, so we are talking about some really significant changes in the government finances," Mr Athow told the BBC.

He added it was impossible to forecast the current year's public finances because of the "high amounts of uncertainty". Tax receipts have fallen heavily, as the Treasury has allowed companies to defer some payments. The amount received from VAT in April was negative, with the government collecting less than was handed back in repayments.

How much does the government spend?

- More than £880bn was spent on services such as defence, policing, the NHS, schools and welfare benefits in the last financial year

- Most of this comes from taxes, which totalled about £840bn last year

- Usually the government spends more money than it has. It borrows money by selling bonds - a promise to repay the money with interest

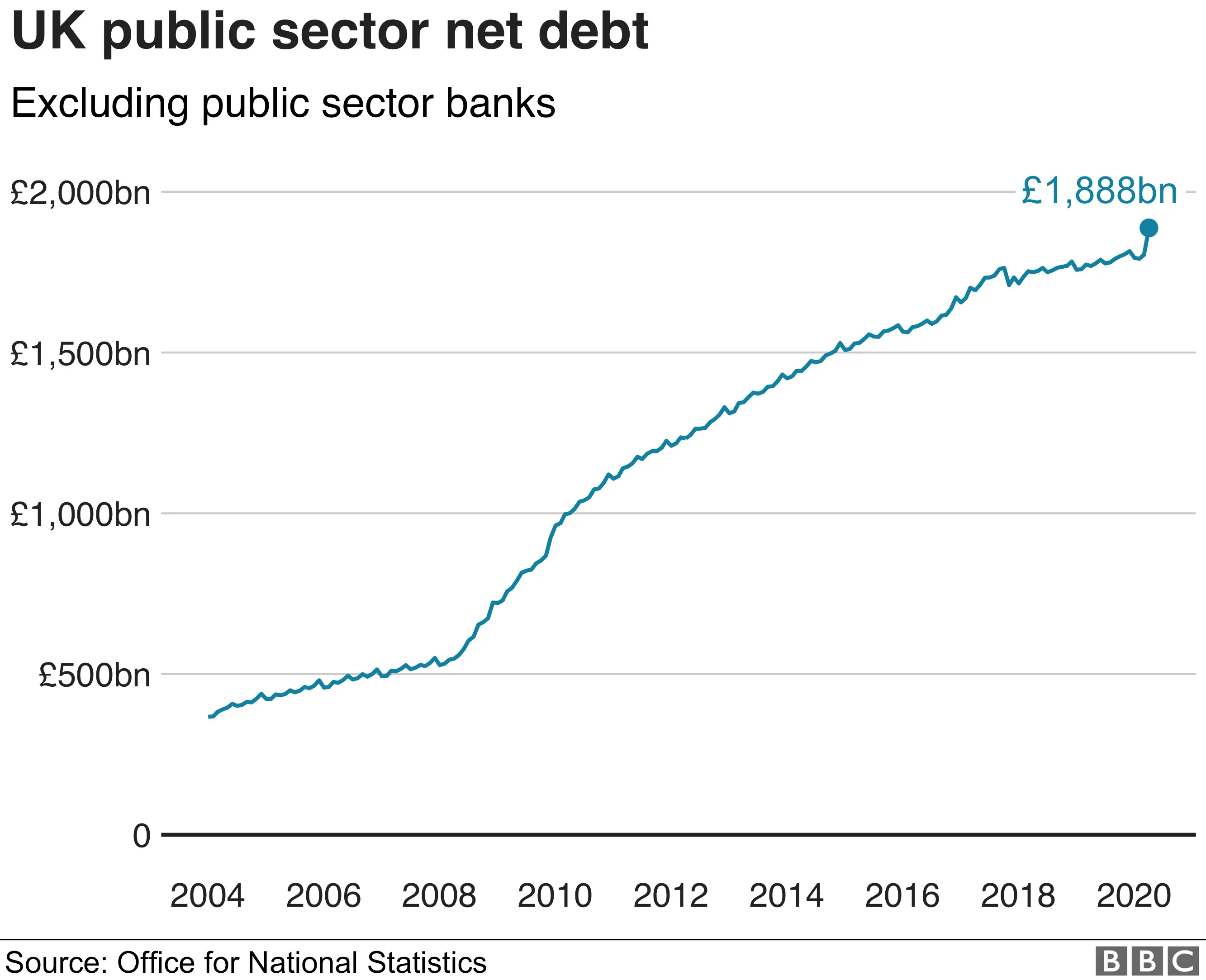

- The total debt has increased over time. It is currently £1.9 trillion - about £28,000 per person in the UK

- Although the debt in cash terms has gone up, money raised from taxes has risen too, which means the debt can be manageable

Meanwhile, borrowing by the state in March 2020 has been revised up by £11.7bn to £14.7bn, the ONS said.

It said this was driven by a reduction in previous estimates of tax receipts and National Insurance contributions.

The surge in borrowing comes after Chancellor Rishi Sunak stepped up financial support for businesses and employees after vast areas of the economy were forced to halt due to the coronavirus lockdown.

After publication of the figures, Mr Sunak said that if the government had not provided financial support, the cost to the economy and people's livelihoods would be much worse.

"Our top priority is to support people, jobs and businesses through this crisis and ensure our economic recovery is as strong and as swift as possible," he said.

"That's why we've taken unprecedented steps to provide lifelines to people and businesses with our furlough scheme, grants, loans and tax cuts."

Buy now - worry later?

For the past decade, the government had been trying to practise strict financial housekeeping, aiming for position where it could cover day-to-day spending with the money form our taxes and eliminate the deficit.

But then the crisis hit - and as the chancellor claims, the schemes put in place have provided a lifeline to tide millions over, to prevent an even bigger economic disaster. It was worth ripping up the rulebook for, he said.

However the bills are mounting, just as the amount received from taxpayers slumped.

This year's deficit could be the equivalent of the biggest slice of our income since the Second World War - and that hole needs plugging.

For the moment, the government has increased its borrowing on financial markets, through bonds, effectively IOUs - but there is a limit to how much it can do so.

Ultimately, economists say taxes will have to rise, or spending cut - the emergency raft will have a price tag which we can't escape.

But the chancellor will have to impose those carefully to avoid jeopardising a recovery. And if he opts for tax hikes, he'll risk breaking some election promises.

'Britain is poorer'

The scale of the economic consequences was underlined on Friday in separate retail sales data from the ONS. These showed that High Street sales crashed last month as shops closed for the lockdown.

It was also announced on Friday that a mortgage payment holiday scheme for homeowners in financial difficulty during the pandemic has been extended for another three months.

As a result of the jump in borrowing, total public sector debt rose to £1,888bn at the end of April - £118.4bn higher than April 2019.

Former chancellor George Osborne told the BBC: "We have to come to terms with the fact that Britain is poorer and the economy is smaller than it would have been."

Asked if the economy would bounce back, he said: "Bounce is the wrong word, but it will recover."

Ruth Gregory, an economist at Capital Economics, described April's borrowing as "alarmingly high", but added that a small easing of the lockdown from 13 May probably meant the government would not have to borrow as much this month.

And despite the pressure on public finances, Charlie McCurdy, a researcher at the Resolution Foundation, said there were no signs the government was struggling to raise money on the financial markets.

"Record low interest rates mean the UK's higher debt burden should remain more than manageable," he said.

- RISK AT WORK: How exposed is your job?

- THE R NUMBER: What it means and why it matters

- LOOK-UP TOOL: How many cases in your area?

- RECOVERY: How long does it take to get better?

- A SIMPLE GUIDE: What are the symptoms?