How the US Federal Reserve sets interest rates

New York Federal Reserve

New York Federal ReserveWith so much of politics, economics, culture - not to mention every other facet of human existence - taking place online, it is startling to realise that such a loose and baggy concept as the "centre of the global economy," can actually be located somewhere real: in a particular grey stone building in lower Manhattan in fact; and within that building, on a particular floor.

It is the open markets desk of the New York Federal Reserve - a trading floor that looks much like any other big open plan office.

But the people working here aren't typing away at the usual sort of office email or message. What they have their hands on is the basic lever of the whole global economy - US interest rates.

Do you pay interest? Probably. Anyone with a mortgage, a car loan, or a credit card does. Do you earn it? Again, it's very likely, if you've ever had money in a savings account.

And if you've studied the statements you get from your bank you'll know that the rate of interest that is paid or earned has a big impact on how much money you are able to spend on other things.

Huw Evans picture agency

Huw Evans picture agencyWhat's true for you is true for the bank, too. How much it costs you to borrow money, influences how much you can afford to spend. How much it costs the bank to borrow money, directly affects how much it's going to charge you for a loan, or how much it's going to pay you on your savings.

And think about those savings. If you're sure you can get a higher rate of return by taking your money out of the bank and putting it into the stock market then usually you will.

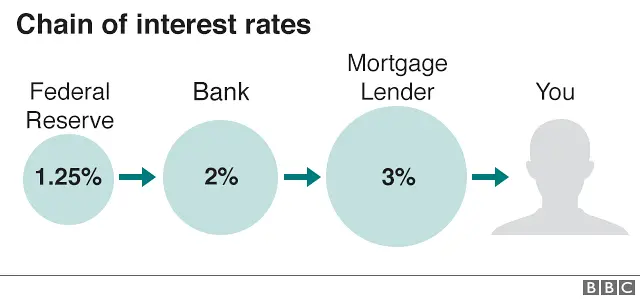

In this way the entire US economy can be seen as one long chain of interest rates.

If it is, then at the start of that chain, is the US's central bank, the Federal Reserve. The interest rate set by the Fed is the one to which almost every other interest rate in the world is linked.

You may have seen changes in that rate in the news. They happen in Washington and are decided by the Federal Open Markets Committee (FOMC), usually accompanied by a jargon-filled press conference by the chair of the Federal Reserve

Getty Images

Getty ImagesBut carrying out the policy of the FOMC, is something that's largely the job of the Open Market Desk in the New York Fed.

All of the big commercial banks in the US hold reserves at the Federal Reserve. Reserves are the money banks have to keep on hand in case too many people try to withdraw their money at the same time.

The key US interest rate is what is known as the Federal funds rate. It's the rate of interest that banks earn when they lend their excess reserves to each other.

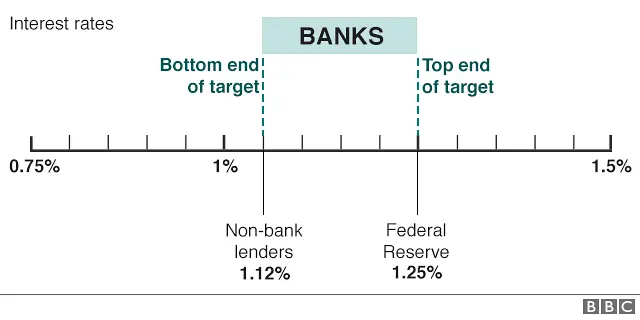

The target for that rate is what the FOMC in Washington decides on at its regular meetings. But making that target into an effective rate is where the Open Markets desk comes in. When the FOMC issues its statement it identifies a range for the federal funds rate. Currently it's between 1-1.25%.

The simplest method of hitting the target is simply to pay the banks interest on their reserves at the rate at the top of the range. Since banks are obliged to try and make money for their shareholders they're not in the business of lending their money out at a lower rate than they can get for just leaving it in their reserves.

The problem is that the banks can borrow reserve funds from other big financial players who are not part of the Federal Reserve System - money market funds for example, or the government sponsored organisations, that play a big role in America's housing market.

And because they're not part of the Federal Reserve System and keeping reserves at the Fed, they are sometimes willing to lend reserve funds to the banks at a rate below that at which the Fed is paying interest to the banks for their reserves.

What the open markets desk does then is offer to borrow money from those non-bank lenders at a rate at the bottom end of the target. Again, no-one works to lose money, so this creates another floor for the federal funds rate, which therefore sits between the two ends of the range.

CHRIS RATCLIFFE

CHRIS RATCLIFFEAnd remember we're all links in a chain of interest rates. If your bank has to pay 1.25% interest on the money it needs to keep its reserve funds full, it's going to charge you a higher rate on your mortgage in order to make a profit, or pay you a lower rate on your savings.

So when the amount of money you have left over after you've paid interest on your loans changes, or when the amount of interest your savings earns changes, you're feeling the effects of the work of the traders at the New York federal reserve.

Beyond that, since the US economy is the biggest in the world, and so are its financial markets, borrowers and investors everywhere are living in a world directly shaped by the men and women on the open markets desk in New York.